Award-winning PDF software

Miami-Dade Florida Form 1041-T: What You Should Know

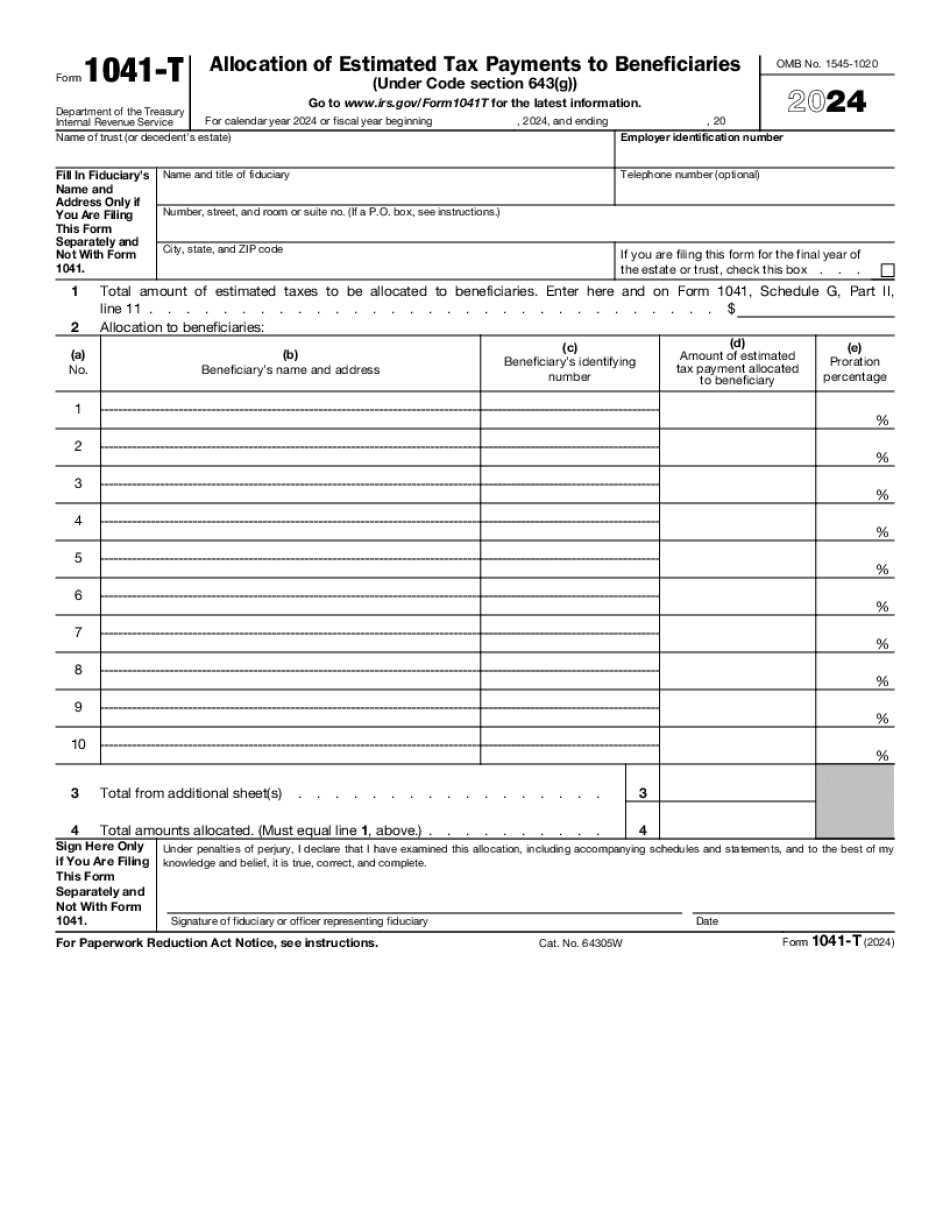

If you or your estate has not met the requirement to file before February 25 of the year in which you are electing to have your taxes allocated to beneficiaries, the trust or estate should file a new paper in the IRS' e-filing system to elect in advance. Trusts and estates may not elect to allocate the full amount of the death tax on the estate or the trust, as a result of one of two trust or estate income tax consequences: Income is subject to death tax on that income. Other trust or estate income is not taxed on that income subject to death tax if the trust or estate does not elect to allocate the full amount of the death tax on the estate or trust, as a result of one of the following trust or estate income tax consequences: (1) You and your spouse have met all the other qualifications, such as the age, residence and filing status for the year, to claim the exemptions that would prevent the estate or trust from taking the full death tax credit; or (2) The estate or trust does not take any of the allowable deductions, exclusions, or credits, such as for expenses, that reduce or exclude income, and no amount of the capital gains tax you would take, even with the estate or trust's election, is included in its total income. (Tax law rules have evolved in recent decades to make sure the tax credit provided by the tax code is not inappropriately used with respect to distributions to a non-eligible beneficiary.) You are not married to the decedent. You were not the surviving spouse at the time of the decedent's death. There will either be not enough assets to meet the estate's credit on the estate taxes or all the estate's assets will be taxed. To make sure the estate or trust is not subject to an election to allocate the full death tax on the estate or trust and will not otherwise be subject to this rule, the decedent's final will or the trust's executor or administrator must ensure that the trust elects to avoid the rule. The executor or administrator should make this election on the decedent's final will, in accordance with the instructions and notices of the trust as to the process for making the election. The estate's or trust's election will not be retroactive.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete Miami-Dade Florida Form 1041-T, keep away from glitches and furnish it inside a timely method:

How to complete a Miami-Dade Florida Form 1041-T?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your Miami-Dade Florida Form 1041-T aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your Miami-Dade Florida Form 1041-T from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.