Award-winning PDF software

Form 1041-T for Murrieta California: What You Should Know

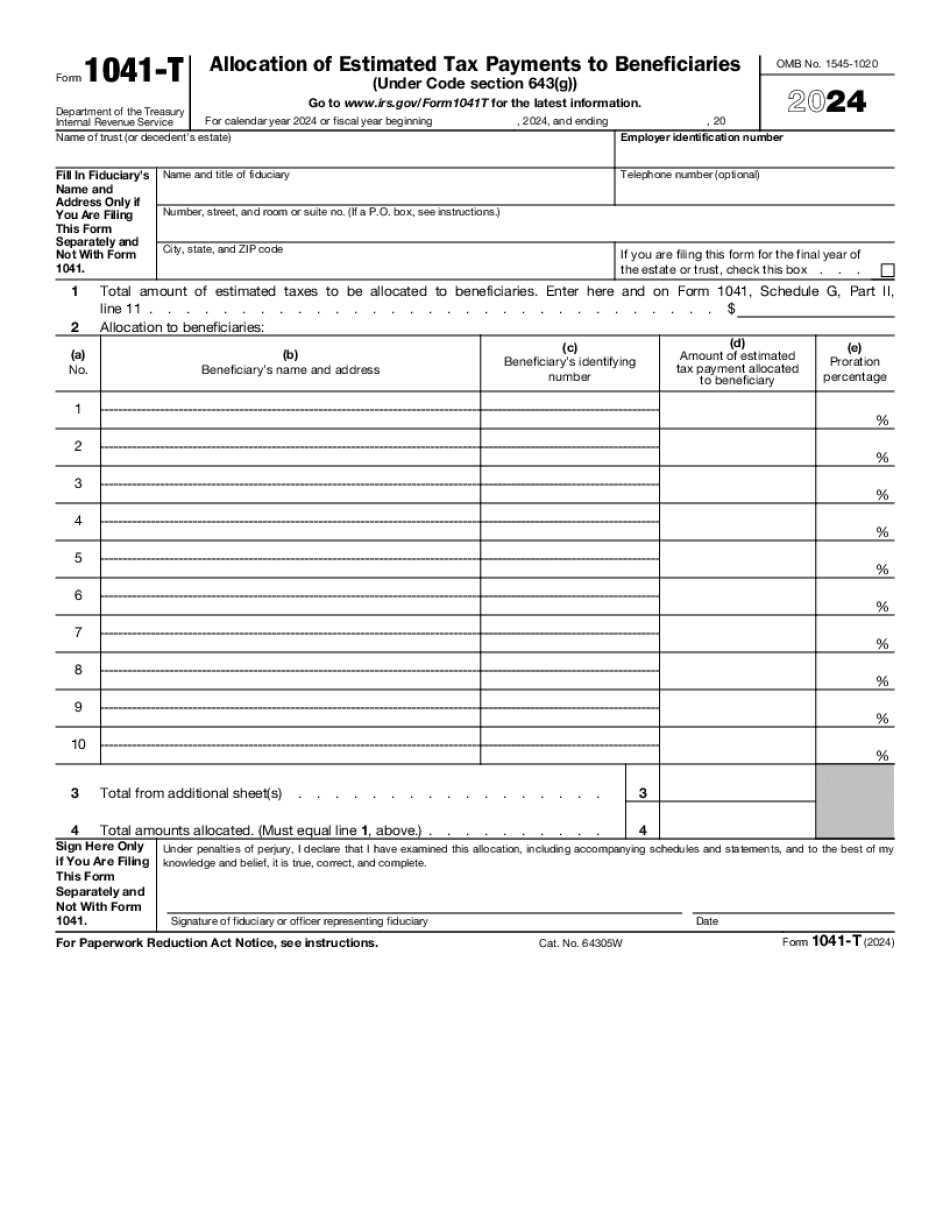

There are Form 1041 Allocation of Estimates of Tax Payments to be Made To Beneficiaries Must be Made During Future Tax Year Only if a Trust or Estate Would Not Qualify for a Deductions Exception, or a Deductions Exceptions Not Applicable Under A Self-contained Plan — Explanations Form 1041 Allocation of Estimated Tax Payments to Beneficiaries is only made when a trust or estate would not, under the terms of its trust agreement (whether filed) qualify for a deduction for estimated tax payments. A trust or estate may not make an election under this section. The only time an estate or trust may make an election under this section is, without limitation, to establish a deduction for taxes that would not be deductible under section 537 or section 542, (as defined in Section 1546 of the Internal Revenue Code), for the taxable year that includes the trust's (or the decedent's) death. A tax year begins on the date of payment or receipt of income or with respect to estate income, whichever is later. In general, trust income and trust taxable income that would be deductible must be distributed to beneficiaries before the trust's (or the decedent's) death to provide the trust with sufficient income to fund all of its trust income-based and nondeductible expenses for that taxable year. However, a trust cannot make an allocation election under this section to allocate the total amount of tax paid to its beneficiaries if it cannot reasonably be expected to meet the distribution requirement to provide the trust with sufficient income to meet all of its trust expenses for that year (other than distributions required for its posthumous relief of its beneficiaries). However, a trust may make an allocation election under this section if it has made a certification under section 6103(f) of the Internal Revenue Code under the condition that it is unable to distribute the trust's earnings and profits to its beneficiaries prior to the trust's (or the decedent's) death. If it has not made a certification under section 6103(f) in the 10-year period ending on the trust's (or the decedent's) death, then the trust may make an allocation election.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete Form 1041-T for Murrieta California, keep away from glitches and furnish it inside a timely method:

How to complete a Form 1041-T for Murrieta California?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your Form 1041-T for Murrieta California aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your Form 1041-T for Murrieta California from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.