Okay, for this video, I wanted to go over a very simple example of how to complete a Form 1041 trust tax return for a revocable non-grantor trust. Trust returns can get incredibly complicated, so I'm going to use a very simple example with a little bit of income and expenses, one beneficiary, and show you how the fact pattern works with the return and the basic sections of the return that you need to complete. Moving on to the K1s as well, I have the sample 1041 in front of us. We'll go through all the relevant fields here, and I also have a sample fact pattern to review. This is the information we're going to use to populate the 1041 tax return. Now, let's look at the fact pattern. We have Jane Smith, a U.S. taxpayer and grantor, who wants to form an irrevocable non-grantor trust for the benefit of her only daughter, Daughter Smith. Jane has a lawyer draft up a trust agreement, effective February 1, 2021, appointing John Doe Fake Trust Company Inc as the trustee for the trust. In this case, the trust is using a corporate trustee, which means it's an actual business. However, a trust can also appoint an individual as a trustee. You can have either or even multiple trustees, depending on your preferences. But in this example, we have only one trustee, one fiduciary, and that's John Doe Fake Trust Company Inc. After that is done, a brokerage account is opened for the trust. Jane, as the grantor, puts $14,000 in cash into the brokerage account. The trustee then invests those cash proceeds into dividend-paying ETF stocks. During the year, if we look at the brokerage account, we see that a 1099 is issued at the end of the year, showing that $840 of...

Award-winning PDF software

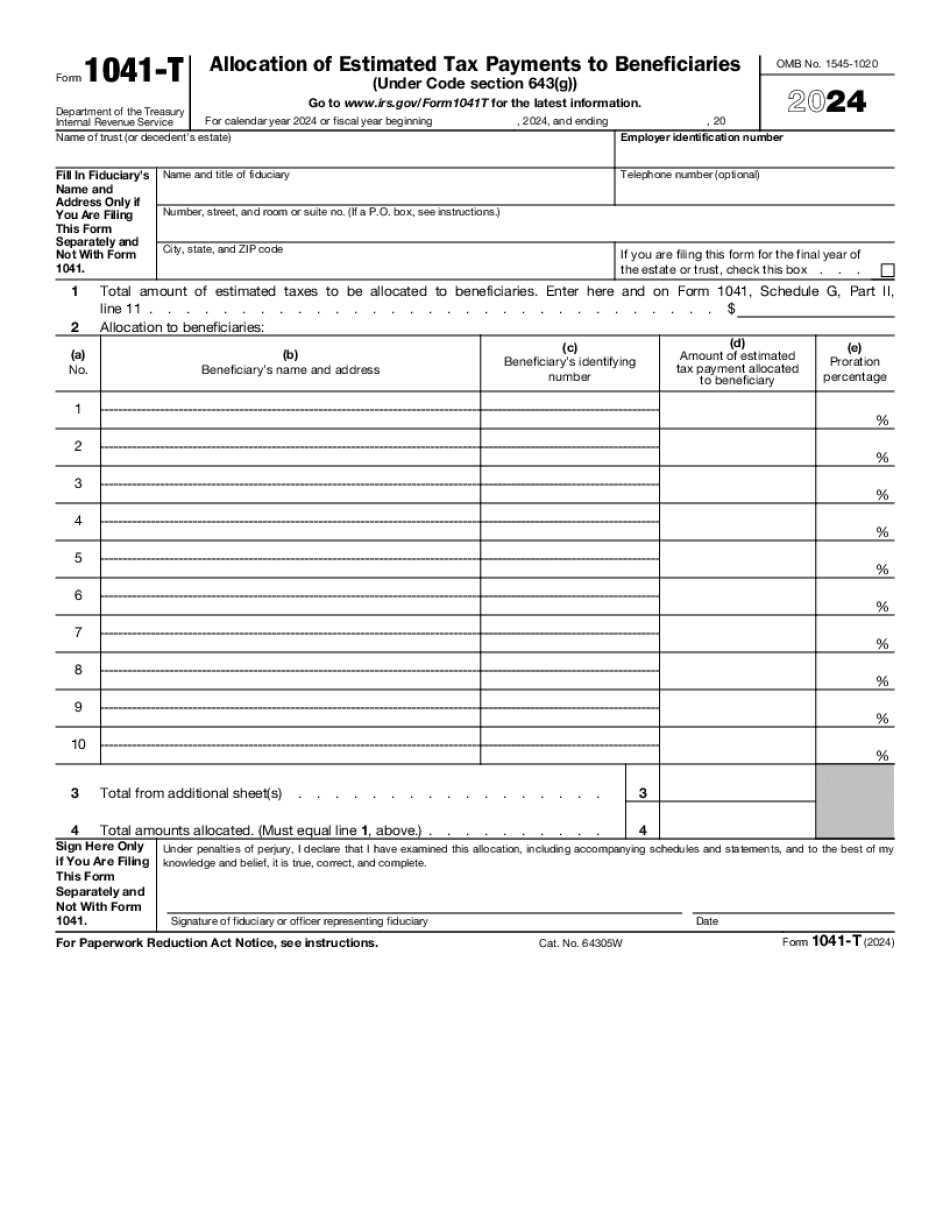

About Form 1041-T, Allocation Of Estimated Tax Payments To: What You Should Know

IRC § 643(g) will help avoid double taxation. When an estate or trust files an IRC § 643(g) election with IRS, it is treated as a. To maximize the amount of relief available to you, filing this form early will benefit you. You must file it in time for your scheduled filing. Form 8582 or 8582-S ‐ Tax Paid on Shareholder Interest In the case of a trust or estate that has more than one surviving spouse, you should report the income from the property of the decedent who has died within the period that starts with the date on which the decedent meets with his or her property and ends with the date on which the property is sold or transferred. Sep 19, 1997—A trust was created to distribute the decedent's estate. It had three beneficiaries. It also recorded an interest in all the assets of the estate in the name of the trustee. The trust's representative, the person that holds and transfers all the trust's properties, is the executor. The representative also collects and pays all the interest income received that is not taxable on a return of capital. The representative is the designated fiduciary. Form 1041, Form 1041-T, or Form 3950 If a trust or estate has assets, and it is subject to taxation, the trust or the estate (trust or estate) should file either a, the actual interest income, or a, the tax-exempt interest income. If the trust or the estate uses either of these methods, the following rules apply: For the actual interest income, all earnings and profits attributable to the assets of the trust or estate must be reported; in this case, the actual interest income is reported on Form 1041, as well as on Form 1041-T for the estate and on Form 3950 for each of the trust's beneficiaries. This type of information is also posted on this IRS website. For the tax-exempt interest income, only the interest income of the trust is subject to tax. However, if the trust is the custodian for the decedent's entire estate as evidenced by the decedent's death certificate and other documentation issued by the hospital, nursing home, or other medical provider, the assets of the trust must be reported on Form 8582 or Form 8582-S, as appropriate. This type of information is also posted on this IRS website.

Online systems enable you to to arrange your doc management and supercharge the productivity of one's workflow. Comply with the fast guidebook with the intention to comprehensive About Form 1041-T, Allocation of Estimated Tax Payments to, prevent errors and furnish it in the timely method:

How to finish a About Form 1041-T, Allocation of Estimated Tax Payments to internet:

- On the web site while using the form, click Launch Now and go towards editor.

- Use the clues to complete the related fields.

- Include your individual information and facts and phone info.

- Make guaranteed you enter suitable information and quantities in applicable fields.

- Carefully test the information with the variety also as grammar and spelling.

- Refer to assist section when you've got any queries or tackle our Aid crew.

- Put an digital signature in your About Form 1041-T, Allocation of Estimated Tax Payments to with the assistance of Indication Device.

- Once the shape is finished, push Done.

- Distribute the all set sort through e-mail or fax, print it out or help save on the product.

PDF editor will allow you to definitely make changes towards your About Form 1041-T, Allocation of Estimated Tax Payments to from any online world related product, customize it in keeping with your requirements, indication it electronically and distribute in various strategies.

Video instructions and help with filling out and completing About Form 1041-T, Allocation Of Estimated Tax Payments To