It's critical when deciding capital for trust purposes that the trustee determines if the intended recipient is a beneficiary. If the distribution is made to someone who is not a beneficiary at that time, it is ineffective for trust purposes and invalid. This means that the trust income or capital has not been distributed effectively, resulting in unintended accumulation of income and no distribution. Consequently, the trustee will have to pay taxes on that amount at the highest marginal rate. From a tax planning perspective, what the trustee believed they were achieving will not work from a trust law point of view. Furthermore, it is important for the beneficiaries to be the sole recipients of distributions from the trust. If other beneficiaries miss out on receiving their allocated amounts, they have the right to sue the trustee for an invalid distribution to someone who shouldn't have received it. However, the most crucial point to take from this is that practitioners must thoroughly examine their trustees to ensure that the individuals receiving income or capital are indeed beneficiaries. The long-term consequences in terms of taxation can be devastating. In case of a distribution failure and subsequent assessment by the Commissioner, there will be amended assessments to be paid, along with possible interest and penalties on unpaid tax. Therefore, before making any distributions or passing resolutions, the first step each year should be to determine that the intended recipients are actually beneficiaries. There have been cases where, for instance, the principal of the Trust has remarried, assuming their new spouse to be a beneficiary. However, if she is not, any distributions made to her would be invalid, resulting in reassessments. Overall, it is crucial to accurately divide the text into sentences and correct any mistakes to ensure clarity and understanding.

Award-winning PDF software

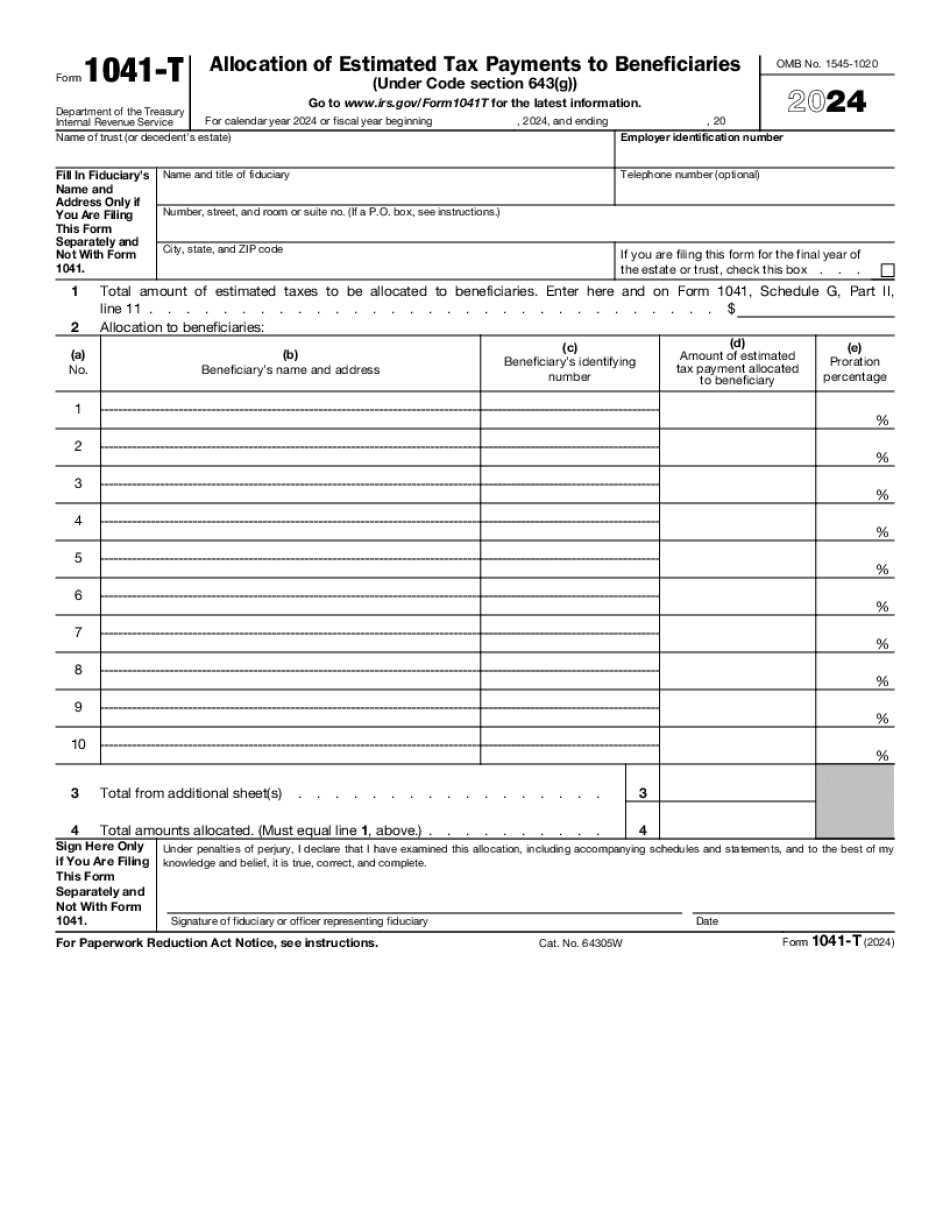

Withholding on trust distributions Form: What You Should Know

Foreign income The following expenses are included in gross income only if they were incurred within one year of the date of the trust creation (and not earlier). Foreign capital gain or loss Real property sales, rentals, and leases Business transactions that qualify under Section 853 of the Code, Tax exclusions Certain items not included in gross income (such as distributions that are not eligible for a credit against tax liability, distributions made to any trust that is not taxed under Section 7046 of the Code, distributions that are not eligible for a credit against income tax) The 1022(f)(2) election must be made by the reporting trust. The following income is not considered income but must be included on Form 1040, W-2 form, or 1099: Any amount received from a granter trust. Income from the sale of land. Fiduciary Information Fiduciaries will need to be familiar with the types of tax rules that apply to them: Tax Forms | Tax Forms (1) | (2) | (4) | (5) | (3) | (2) | (4) | (7) | (9) | (3) | (7) | (9) | (16) The following tables list all the tax forms, schedules and instructions: Schedule A — Information, Statement, and Instructions for Executors and Trustees Form 1040 — U.S. Income Tax Return Instructions for reporting distributions to trusts, estates, and designated beneficiaries (Form 1033) from a retirement plan; Form 1045(B) — U.S.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 1041-T, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 1041-T online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 1041-T by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 1041-T from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Withholding on trust distributions